House Price Estimate UK: How To Value Your Home Accurately

Welcome to our complete guide to obtaining a house price estimate UK, where you will learn how property valuations work, what factors influence house prices, and how to determine the most accurate value for your home. Whether you are planning to sell, buy, remortgage, invest, or simply stay informed about your property’s worth, understanding how house price estimates are calculated can help you make smarter financial decisions. In this guide, we explore the tools, data, and professional valuation methods used across the UK, explain the strengths and limitations of online estimates, and share practical insights to help you assess your property’s value with greater confidence and accuracy.

A house price estimate UK is an approximate valuation of a property based on factors such as recent local sales, property size, condition, location, and current market trends. Homeowners can obtain estimates through online valuation tools, estate agents, surveyors, or mortgage lenders to better understand a property’s current market value.

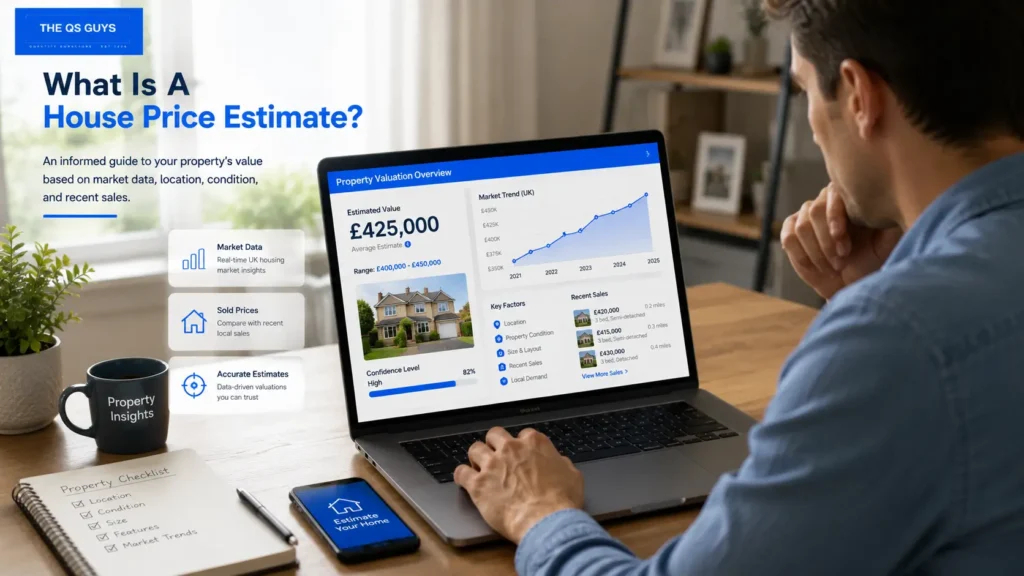

What Is A House Price Estimate?

A house price estimate is a guide to what a property may be worth in the current market. It helps homeowners, buyers, and investors understand a likely price range before making important property-related decisions. While it can give a useful starting point, it should be treated as an informed estimate rather than a guaranteed sale price.

Understanding Property Valuations

A house price estimate is an approximate calculation of a property’s value based on factors such as location, property size, condition, recent local sales, and wider housing-market trends. In the UK, these estimates may come from online valuation tools, estate agents, property platforms, or local-market data.

The main difference between a house price estimate and a formal property valuation is the level of detail and professional responsibility involved. An estimate is usually designed to give a quick guide, while a formal valuation is often completed by a qualified surveyor, mortgage lender, or property professional for legal, lending, tax, or financial purposes.

- House price estimate: A general guide that helps you understand what your home may be worth based on available property data.

- Formal property valuation: A more detailed assessment usually carried out by a professional for official, legal, or mortgage-related reasons.

- Online estimate: A fast, data-led figure that can be useful but may not fully account for renovations, property condition, or unique features.

- Estate-agent appraisal: A market-focused opinion that considers buyer demand, local competition, and recent selling activity.

For example, an online tool may estimate a home’s value using nearby sold prices, but it may not know that the property has a new kitchen, upgraded insulation, off-street parking, or structural issues. This is why estimates are helpful, but they work best when combined with local knowledge and professional advice.

Why House Price Estimates Matter

A house price estimate matters because property decisions often involve large financial commitments. Whether you are selling, buying, remortgaging, planning inheritance matters, or reviewing an investment, knowing a realistic value can help you avoid costly mistakes.

- For sellers, a reliable house price estimate can help set a sensible asking price. Pricing too high may cause the property to sit on the market for too long, while pricing too low could mean losing money. A well-researched estimate gives sellers a clearer starting point before speaking with estate agents or listing their home.

- For buyers, house price estimates help assess whether a property is fairly priced. By comparing the asking price with recent local sales and market conditions, buyers can make stronger offers and avoid overpaying.

- For homeowners who are remortgaging, an updated estimate can help show how much equity may be available. This can affect borrowing options, loan-to-value ratios, and future financial planning.

House price estimates can also be useful for estate planning and inheritance. Families may need a realistic property value when managing assets, preparing probate information, or making long-term financial decisions.

For property investors, estimates support smarter decision-making. They help compare potential returns, assess capital-growth opportunities, and understand whether a property is priced appropriately for the local market.

- Selling a property: Helps guide the asking price and supports a stronger sales strategy.

- Buying a home: Allows buyers to compare the listed price with local-market evidence.

- Remortgaging: Helps homeowners understand equity and possible borrowing options.

- Estate planning: Supports financial planning, inheritance discussions, and asset reviews.

- Investment decisions: Helps investors assess value, risk, and long-term growth potential.

A good estimate gives you confidence, but the strongest decisions usually come from comparing several sources rather than relying on one figure.

House Price Estimate vs Market Value

A house price estimate and market value are closely related, but they are not always the same. A house price estimate is an informed guide, while market value is the price a willing buyer is likely to pay in real conditions at a specific point in time.

Asking prices can also differ from actual selling prices. A seller may list a property higher to allow room for negotiation, or they may price it lower to attract more interest. The final sale price depends on buyer demand, competing properties, mortgage conditions, property condition, and how motivated both parties are.

For example, two similar homes on the same street may receive different offers if one has been recently renovated and the other needs major repairs. Even small details such as garden size, parking access, energy efficiency, and presentation can influence the final price.

Market conditions also play a major role. When demand is high and there are fewer homes available, properties may sell above estimate or asking price. When demand is weaker, buyers may negotiate harder, and homes may sell below the initial guide price.

- Asking price: The amount a seller lists the property for, which may be higher or lower than the final sale price.

- Estimated value: A calculated guide based on data, comparable sales, and property details.

- Market value: The realistic price a buyer may be willing to pay in the current market.

- Final sale price: The amount agreed between buyer and seller after negotiation.

Understanding these differences helps homeowners, buyers, and investors read property figures more accurately. A house price estimate UK search can give a useful starting point, but true market value is shaped by real buyer behaviour, local demand, and the specific condition of the property.

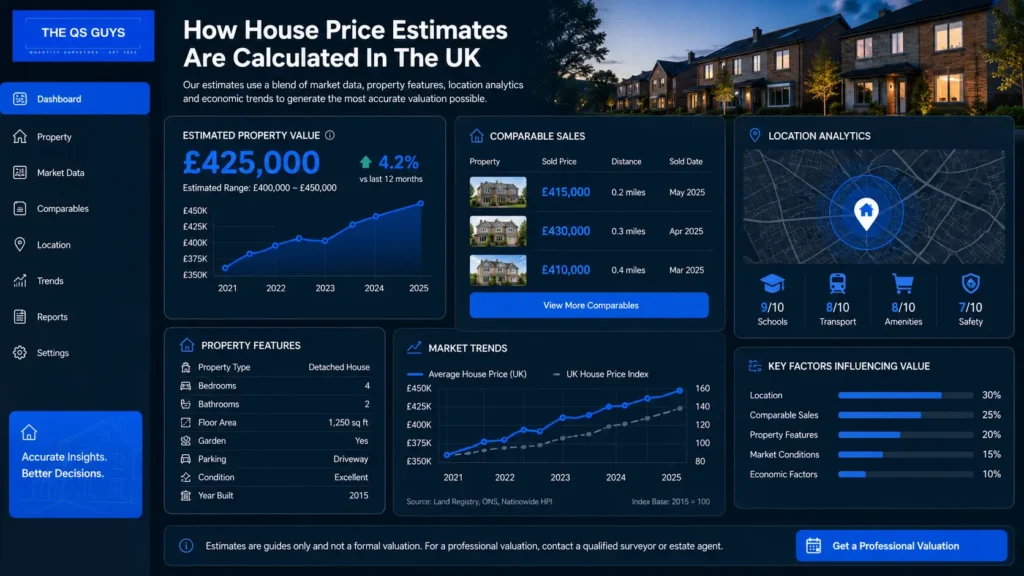

How House Price Estimates Are Calculated In The UK

A house price estimate in the UK is usually calculated by looking at a mix of verified property data, local market activity, property-specific features, and wider economic conditions. No single factor gives the full picture, which is why the most reliable estimates compare several sources before arriving at a realistic market value.

Recent Sold Property Data

Recently sold property data is one of the strongest starting points for calculating a house price estimate because it shows what buyers have actually paid for similar homes. In the UK, this often includes Land Registry data, which records completed property sales across England and Wales. This information is useful because it reflects real transaction prices rather than asking prices, which can sometimes be higher than what a property eventually sells for.

Comparable property sales, often called comparables, are also important. A strong comparison looks at homes with similar size, age, condition, layout, and location. For example, a three-bedroom semi-detached home should usually be compared with other three-bedroom semi-detached homes in the same area, not with larger detached houses or smaller flats.

Local market trends also influence the estimate. If similar homes in the area are selling quickly and close to asking price, the estimate may be stronger. If properties are sitting on the market for longer or being reduced, this may suggest softer demand.

- Land Registry Data: This gives a reliable record of actual sold prices and helps remove guesswork from the valuation process.

- Comparable Sales: Similar recently sold homes provide a practical benchmark for what buyers are willing to pay.

- Local Trends: Changes in buyer demand, average sale times, and price reductions can all affect the final estimate.

Property Features That Affect Value

The physical features of a home play a major role in any house price estimate UK homeowners receive. Buyers usually compare homes based on space, layout, condition, and convenience, so even small differences can affect value.

The number of bedrooms and bathrooms is one of the clearest value indicators. A home with an extra bedroom or second bathroom may appeal to a larger group of buyers, especially families or remote workers who need flexible space. Property size also matters, particularly the total floor area and how usable the layout feels.

Condition is another key factor. A well-maintained property with modern upgrades, such as a renovated kitchen, updated bathroom, improved insulation, or newer heating system, may achieve a higher estimate than a similar home needing repairs. However, upgrades need to suit the local market. Over-improving a property beyond what buyers expect in the area may not always return the full investment.

Outdoor space can also increase value, especially where gardens, patios, or low-maintenance outdoor areas are in demand. Parking and garages are particularly valuable in busy towns, commuter areas, and locations where street parking is limited.

- Bedrooms And Bathrooms: More usable rooms can improve buyer appeal and increase the estimated value.

- Property Size: Larger homes often attract higher valuations, but layout and usable space matter as much as square footage.

- Condition And Upgrades: Modern, well-kept homes usually estimate higher than properties needing immediate work.

- Outdoor Space: Gardens, patios, and private outdoor areas can add value, especially for families and lifestyle-focused buyers.

- Parking And Garages: Off-street parking can be a major value factor in high-demand residential areas.

Location And Neighbourhood Factors

Location is often one of the biggest influences on a property estimate because buyers are not only purchasing the home itself, but also the surrounding lifestyle, convenience, and long-term potential of the area.

School catchment areas can have a strong effect on house prices, especially for family homes. Properties close to well-rated schools may attract more competition, which can push values higher. Transport links also matter, particularly for commuters. Easy access to train stations, bus routes, motorways, and city centres can make a home more desirable.

Local amenities such as shops, parks, healthcare services, restaurants, and leisure facilities can support stronger demand. A property in a well-connected neighbourhood with everyday conveniences nearby will often be more attractive than a similar home in a less accessible location.

Crime rates and overall neighbourhood reputation can also affect value. Buyers often research safety, noise levels, traffic, and general area appeal before making an offer. Future developments may raise or lower estimates depending on their impact. A new transport link or town-centre regeneration project may increase demand, while disruptive construction or overdevelopment may make some buyers cautious.

- School Catchments: Homes near popular schools can attract stronger interest from family buyers.

- Transport Links: Good commuter access can increase demand and support higher property values.

- Local Amenities: Shops, parks, healthcare, and leisure options make an area more convenient and desirable.

- Crime Rates: Safety and neighbourhood reputation can influence buyer confidence.

- Future Developments: Regeneration, infrastructure upgrades, or major construction projects can affect long-term value.

Current UK Housing Market Conditions

A house price estimate is not fixed because the wider UK housing market can change over time. Even if a property remains the same, its estimated value may rise or fall depending on demand, borrowing conditions, and regional trends.

Supply and demand are central to property pricing. When there are more buyers than available homes, prices often rise. When there are fewer active buyers or more properties for sale, sellers may need to price more competitively.

Interest rates also influence house price estimates because they affect mortgage affordability. When borrowing costs are higher, some buyers may reduce their budgets, which can soften demand. When rates are lower or more stable, confidence may improve, particularly among first-time buyers and movers.

Regional market variations are also important. Property values in London, the South East, northern England, Scotland, Wales, and Northern Ireland can move differently depending on local employment, wages, housing supply, and buyer demand. A national house price trend may not always reflect what is happening in a specific town or postcode.

Economic influences such as inflation, wage growth, employment levels, and consumer confidence also shape the market. Buyers are more likely to act when they feel financially secure, while uncertainty can slow decision-making.

- Supply And Demand: Strong buyer competition can increase estimates, while low demand may reduce them.

- Interest Rates: Mortgage affordability has a direct impact on what buyers can realistically offer.

- Regional Differences: UK property markets vary widely, so local data is more useful than national averages alone.

- Economic Conditions: Employment, inflation, and confidence all influence how active the housing market feels.

A reliable house price estimate works best when it combines accurate sold-price data, property-specific details, local knowledge, and current market context. Online tools can provide a useful starting point, but the most realistic valuation usually comes from comparing multiple sources and understanding how real buyers view the property in today’s market.

Ways To Get A House Price Estimate In The UK

There are several ways to obtain a house price estimate in the UK, ranging from free online tools to detailed professional valuations. The right option depends on your goals, whether you are preparing to sell, considering a remortgage, managing an inheritance matter, or simply curious about your property’s current value. Understanding how each valuation method works can help you choose the most suitable approach and gain a more accurate picture of your home’s worth.

Online House Valuation Tools

Online house valuation tools have become one of the most popular ways to get a quick property estimate. These platforms use large amounts of market data and technology to generate an estimated value within minutes.

How Automated Valuation Models Work

Most online valuation tools rely on Automated Valuation Models (AVMs). These systems analyse available property and market data to estimate what a home may be worth in the current market.

AVMs typically consider factors such as:

- Recent Sales Data: Comparable properties that have recently sold in the local area.

- Property Characteristics: Details such as property type, floor area, number of bedrooms, and number of bathrooms.

- Location Information: Nearby amenities, transport links, schools, and local demand.

- Market Trends: Current housing market conditions and regional price movements.

By comparing thousands of similar properties and historical transactions, the system produces an estimated value. While these estimates can provide a useful starting point, they cannot account for every unique feature of a property.

Benefits and Limitations

Online valuation tools offer convenience and accessibility, making them attractive for homeowners seeking a quick estimate.

Benefits include:

- Speed: Results are often available within seconds.

- Convenience: No appointments or property inspections are required.

- Cost-Effective: Most online valuation tools are free to use.

- Market Snapshot: Provides a general understanding of current market positioning.

However, there are important limitations to consider:

- No Physical Inspection: The tool cannot assess the condition of the property.

- Limited Renovation Data: Recent upgrades or extensions may not be reflected.

- Unique Properties: Unusual or luxury homes may be difficult to value accurately.

- Data Dependence: Accuracy relies heavily on available local sales information.

For this reason, online estimates should generally be viewed as a starting point rather than a final valuation.

Estate Agent Valuations

Estate agent valuations are a common choice for homeowners considering selling their property. Unlike automated tools, estate agents assess the property in person and combine market data with local knowledge.

What to Expect During an Appraisal

An estate agent appraisal typically involves a visit to the property. During the inspection, the agent evaluates various aspects that may influence the property’s value.

They will usually assess:

- Property Condition: Overall maintenance, presentation, and structural condition.

- Interior Features: Room sizes, layout, modernisation, and finishes.

- Exterior Appeal: Gardens, driveways, parking, and kerb appeal.

- Local Market Activity: Current buyer demand and competing listings.

After reviewing these factors, the agent will provide an estimated market value and may suggest a recommended asking price if the property is being prepared for sale.

Advantages of Local Market Expertise

One of the greatest strengths of an estate agent valuation is local market knowledge. Experienced agents understand buyer behaviour and market trends that may not be visible through automated systems.

Benefits of local expertise include:

- Neighbourhood Insight: Understanding what buyers are currently looking for in the area.

- Pricing Strategy: Recommendations based on active market conditions.

- Awareness of Local Demand: Knowledge of schools, transport projects, and community developments.

- Comparable Property Analysis: Access to recent sales and buyer feedback.

This local perspective can often produce a more realistic valuation than an online estimate alone.

Chartered Surveyor Valuations

For situations requiring a formal and independent assessment, a chartered surveyor valuation is often the most reliable option. These valuations are widely respected and are commonly used for legal, financial, and lending purposes.

When a Professional Valuation May Be Needed

A professional valuation may be necessary when significant financial decisions depend on the property’s value.

Common situations include:

- Mortgage Applications: Lenders may require an independent valuation.

- Probate and Inheritance Matters: Accurate property values are often needed for estate administration.

- Divorce Settlements: Property valuations may form part of financial negotiations.

- Tax Purposes: Certain tax calculations may require professional property assessments.

- Property Disputes: Independent valuations can help resolve disagreements regarding value.

In these circumstances, an objective and professionally prepared report provides added confidence and credibility.

RICS Surveyors and Valuation Reports

Many homeowners choose a surveyor who is accredited by the Royal Institution of Chartered Surveyors (RICS). RICS surveyors follow recognised industry standards designed to ensure consistency and accuracy.

A RICS valuation report typically includes:

- Property Inspection: Detailed assessment of the property’s condition and characteristics.

- Market Analysis: Review of relevant sales and local market activity.

- Valuation Methodology: Explanation of how the final figure was determined.

- Formal Written Report: Documentation suitable for lenders, legal professionals, and financial institutions.

Because these reports are produced independently, they are often regarded as one of the most trustworthy forms of property valuation.

Mortgage Lender Valuations

Mortgage lender valuations serve a specific purpose within the lending process. While they may involve an inspection of the property, their primary objective differs from that of a market appraisal.

Purpose of Lender Assessments

When a buyer applies for a mortgage, the lender needs to determine whether the property provides sufficient security for the loan.

The lender’s valuation helps assess:

- Loan Risk: Whether the property supports the amount being borrowed.

- Property Suitability: Confirmation that the property meets lending requirements.

- Market Value Verification: Ensuring the agreed purchase price is reasonable.

Depending on the lender and property type, the assessment may range from a desktop review to a full inspection.

How They Differ From Market Valuations

A mortgage valuation is not designed to provide detailed advice to the buyer or seller. Its primary purpose is to protect the lender’s financial interests.

Key differences include:

- Focus: Mortgage valuations focus on lending risk rather than achieving the highest market price.

- Level of Detail: Reports are generally less comprehensive than independent surveyor valuations.

- Client: The lender is the primary client, not the homeowner.

- Purpose: Intended to support lending decisions rather than guide property transactions.

As a result, the valuation figure provided by a lender may differ from estimates obtained from estate agents or surveyors.

Whether you choose an online tool, an estate agent, a chartered surveyor, or a mortgage lender assessment, each method offers valuable insights into your property’s value. Comparing multiple sources often provides the most balanced understanding, helping you make informed decisions with greater confidence in an ever-changing UK property market.

How Accurate Are Online House Price Estimates?

Online house price estimates can give homeowners a useful starting point, especially when they want a quick view of what their property may be worth in the current UK housing market. However, they should be treated as informed estimates rather than final valuations because accuracy depends on the quality of the data, the type of property, and how recently the local market has changed.

Factors That Improve Accuracy

Online valuation tools tend to be more reliable when there is enough strong, recent, and relevant property data available. The more closely the available data matches your home, the more useful the estimate is likely to be.

- Strong local sales data: Estimates are usually more accurate when there are recent sold prices from similar homes nearby. If several comparable properties have sold in the same area, the tool has a stronger basis for calculating a realistic house price estimate.

- Standard property types: Online estimates often work better for common property types such as terraced houses, semi-detached homes, and flats in built-up areas. These homes are easier to compare because there are usually more like-for-like sales available.

- Stable market conditions: When the property market is steady, online valuation tools can reflect pricing trends more clearly. Sudden changes in interest rates, buyer demand, or local supply can make automated estimates less dependable.

Situations Where Estimates Can Be Less Reliable

Some homes are harder to value using automated tools because they do not fit neatly into standard pricing models. In these cases, a house price estimate UK tool can still be helpful, but it should be supported by local estate-agent advice or a professional valuation.

- Unique or luxury properties: High-end homes, architect-designed houses, period properties, and homes with unusual layouts can be difficult to compare. Their value often depends on features that online tools may not fully understand, such as design quality, views, privacy, or premium finishes.

- Recently renovated homes: If a property has had a new kitchen, extension, loft conversion, or major energy-efficiency upgrade, the online estimate may not reflect the improvement straight away. Many tools rely on historic data, so recent work may be missed unless it has already influenced nearby sale prices.

- Rural properties: Homes in rural locations can be harder to estimate because there may be fewer comparable sales nearby. Land size, access, outbuildings, views, and local demand can all affect value in ways that automated tools may not fully capture.

- Areas with limited sales history: If few properties have sold recently in the area, the estimate may be based on older or less-relevant data. This can make the figure less accurate, especially in changing markets where buyer demand has moved quickly.

Common Mistakes Homeowners Make

Online estimates are most useful when they are treated as one part of the valuation process. Many homeowners run into problems when they rely too heavily on a single figure without checking whether it reflects the real condition, location, and market position of their property.

- Relying on a single valuation source: One online estimate may not give the full picture. It is better to compare several online tools, recent sold prices, and local estate agent feedback before deciding what your home may be worth.

- Comparing with unsuitable properties: A nearby home is not always a good comparison. Differences in size, layout, condition, garden space, parking, lease length, and renovation quality can create major price differences, even on the same street.

- Ignoring local market changes: Property values can shift quickly when buyer demand, mortgage rates, school catchment popularity, or local development plans change. A reliable estimate should be considered alongside current market activity, not just past sales data.

Online house price estimates are valuable for early research, but they work best when combined with real-world insight. For the most accurate view, compare several sources, review recent local sales, and speak with a trusted property professional before making a major buying, selling, or remortgaging decision.

Key Factors That Can Increase Your House Value

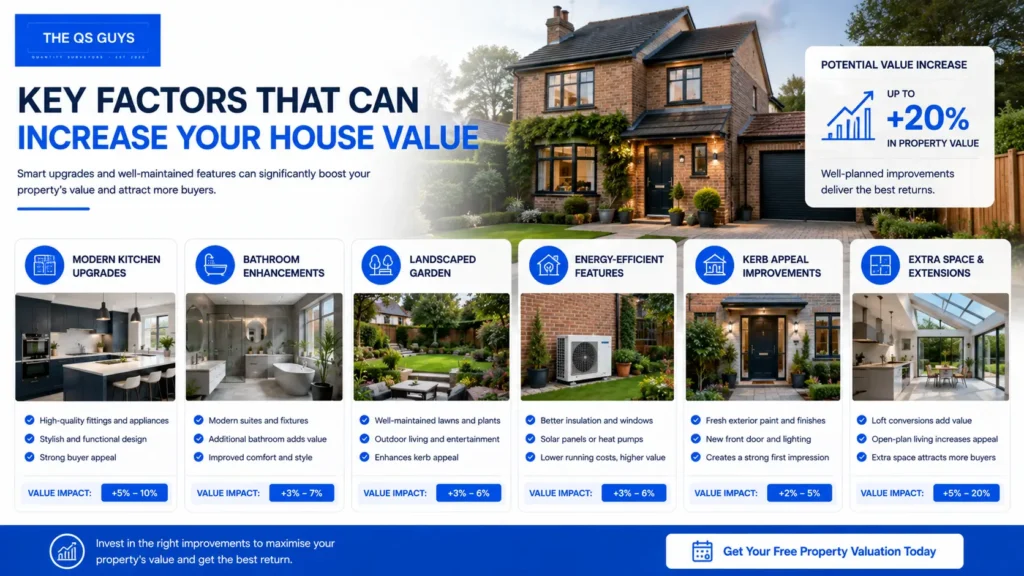

Several practical changes can improve a property’s appeal, comfort, and market value. While every home is different, buyers in the UK often look closely at condition, space, energy performance, and first impressions when deciding whether a property feels worth the asking price. A strong house price estimate is usually supported by improvements that make the home easier to live in, cheaper to run, and more attractive compared with similar properties nearby.

Home Improvements That Add Value

Well-planned home improvements can make a property more desirable, especially when they solve common buyer concerns or improve everyday use. The most effective upgrades are usually those that balance cost, practicality, and long-term appeal rather than focusing only on expensive design choices.

- Kitchen Upgrades: A modern, well-designed kitchen can have a strong influence on buyer interest because it is often seen as the heart of the home. Simple changes such as replacing tired worktops, updating cabinet doors, improving lighting, or adding better storage can make the space feel cleaner and more functional without requiring a full renovation.

- Bathroom Renovations: A fresh, practical bathroom can help improve a property’s overall impression. Buyers often notice signs of wear quickly, so updated fittings, good ventilation, clean tiling, and reliable plumbing can make the home feel better maintained and more move-in ready.

- Energy-Efficiency Improvements: Energy-efficient upgrades are becoming more important as buyers pay closer attention to running costs. Better insulation, double glazing, efficient heating systems, and improved Energy Performance Certificate ratings can make a property more appealing, especially for buyers who want lower monthly bills.

- Loft Conversions And Extensions: Adding usable living space can increase a home’s value when the work is done properly and meets planning and building requirements. A loft conversion, rear extension, or side-return extension can be especially valuable if it creates an extra bedroom, home office, or larger family living area.

Improving Kerb Appeal

Kerb appeal plays a major role in how buyers feel before they even step inside. A property that looks clean, cared for, and welcoming from the outside can create confidence and make the rest of the viewing feel more positive.

- Landscaping: A tidy garden, trimmed hedges, clear pathways, and low-maintenance planting can make the property feel more inviting. Outdoor space does not need to be expensive or elaborate, but it should look usable, safe, and easy to maintain.

- Exterior Maintenance: Buyers often associate poor exterior condition with hidden repair costs. Cleaning gutters, repairing damaged fencing, repainting doors, fixing cracked render, and maintaining windows can help protect the property while improving its appearance.

- First Impressions For Buyers: The entrance area should feel clean, secure, and well cared for. A freshly painted front door, working outdoor light, clear house number, and neat driveway can all help create a stronger first impression during viewings or valuations.

Maintaining Property Condition

A well-maintained property is more likely to receive a stronger house price estimate because it gives buyers fewer reasons to negotiate down. Regular upkeep also helps prevent small issues from becoming expensive problems later.

- Structural Upkeep: Roof condition, walls, flooring, drainage, and foundations all affect buyer confidence. Visible cracks, damp patches, roof leaks, or uneven floors can raise concerns, so it is better to address these issues early and keep records of any professional repairs.

- Preventative Maintenance: Routine maintenance protects the property’s value over time. Servicing boilers, checking electrics, clearing gutters, repairing leaks, and monitoring damp-prone areas can help keep the home in good working order and reduce future repair risks.

- Modernising Outdated Features: Outdated interiors can make a property feel less competitive, even if the structure is sound. Updating old flooring, lighting, heating controls, sockets, paint colours, and storage can make the home feel more current without needing a complete refurbishment.

Increasing your house value is not always about making the biggest changes. The best results often come from practical, well-chosen improvements that make the property feel cared for, efficient, comfortable, and ready for its next owner.

Key Factors That Can Reduce A House Price Estimate

A house price estimate can be affected by more than just the size of the property or the number of bedrooms. Buyers, estate agents, lenders, and valuation tools also consider the home’s condition, the strength of the local property market, and wider location-based factors. Understanding these issues can help homeowners make better decisions before selling, remortgaging, or requesting a formal property valuation.

Property Condition Issues

The physical condition of a property is one of the most important factors that can lower a house price estimate. Even if a home is in a desirable area, visible defects or hidden maintenance problems can reduce buyer confidence and lead to lower offers.

- Damp: Damp can be a major warning sign for buyers because it may point to poor ventilation, leaking pipes, damaged brickwork, or rising moisture from the ground. It can also lead to mould, unpleasant smells, and damage to walls, ceilings, or flooring. If damp is not investigated and repaired properly, it may reduce the property’s estimated value because buyers often factor in repair costs and future risk.

- Structural Concerns: Cracks in walls, uneven floors, subsidence, or movement in the building can affect a property valuation because they may suggest deeper construction-related issues. Surveyors and lenders usually take structural concerns seriously, especially if repairs could be expensive or difficult to complete. Even minor-looking cracks can make buyers cautious if there is no clear explanation or professional report.

- Roof And Foundation Problems: A damaged roof, missing tiles, leaking gutters, or foundation-related movement can lower a house price estimate because these issues affect the long-term stability and safety of the home. Roof repairs and foundation work can be costly, so buyers may negotiate harder or avoid the property altogether. Keeping these areas well-maintained can help protect the home’s market value.

Market And Economic Challenges

A property’s estimated value can also change because of wider market conditions. Even a well-presented home may receive a lower estimate if buyer activity slows down or economic pressure affects affordability.

- Rising Interest Rates: When interest rates rise, mortgage repayments usually become more expensive for buyers. This can reduce the number of people able to afford a property, which may lead to softer demand and lower estimated values. In some areas, higher borrowing costs can make buyers more price-sensitive and cautious.

- Reduced Buyer Demand: If fewer buyers are actively searching in a certain area or price range, properties may take longer to sell. Estate agents and valuation tools often consider buyer demand when estimating value because a slower market can affect realistic selling prices. A home may still be desirable, but reduced competition can limit how much buyers are willing to pay.

- Local Market Downturns: Property values can fall in specific towns, cities, or neighbourhoods even when the wider UK housing market remains stable. Local job losses, oversupply of similar homes, or changes in buyer preferences can all influence valuations. This is why recent sold prices in the immediate area are often more useful than national averages when checking a house price estimate UK.

Location-Related Factors

Location has a major influence on property value, but it is not only about the postcode. Practical day-to-day factors, local convenience, and long-term neighbourhood appeal can all affect how buyers view a home.

- Noise Pollution: Properties close to busy roads, railway lines, airports, nightlife areas, or industrial sites may receive lower estimates if noise affects comfort and privacy. Some buyers may accept noise for a lower price, but others may see it as a deal-breaker. Double-glazing and good insulation can help, but they may not fully remove the impact on value.

- Poor Transport Access: Homes with limited access to public transport, main roads, schools, shops, or workplaces may be less attractive to some buyers. In the UK, transport links often play a strong role in property demand, especially for commuters and families. If a property is difficult to reach or poorly connected, this can reduce its estimated market value.

- Changes In Local Desirability: A neighbourhood’s appeal can change over time due to new developments, school performance, crime levels, business closures, or changes in nearby amenities. Positive changes can increase value, while negative changes may reduce buyer interest. Because local desirability is closely linked to demand, it can have a direct impact on a property’s house price estimate.

A lower house price estimate does not always mean a property has poor potential. Many value-reducing issues can be improved through repairs, maintenance, better presentation, or expert advice before selling. By understanding the factors that affect valuation, homeowners can make informed decisions and take practical steps to protect or improve their property’s market appeal.

How To Get The Most Accurate House Price Estimate

Getting an accurate house price estimate involves more than checking a single online valuation tool. Property values are influenced by a combination of market conditions, location, property features, and buyer demand, which means no single source can provide a completely precise figure in every situation. The most reliable approach is to gather information from multiple trusted sources, review recent market activity, ensure your property’s details are current, and seek professional guidance when necessary. Taking these steps can help you develop a realistic understanding of your home’s potential market value.

Compare Multiple Valuation Sources

One of the most effective ways to improve the accuracy of a house price estimate is to compare information from several valuation methods. Different sources use different data sets and valuation models, so reviewing multiple opinions provides a more balanced and informed perspective.

Online Tools

Online valuation tools are often the quickest starting point for homeowners. These tools use automated valuation models that analyse property records, local sales data, and market trends to generate an estimated value.

- Convenient access: Most online tools provide instant estimates without requiring an appointment or inspection.

- Market overview: They can offer a useful snapshot of current market conditions in your area.

- Initial benchmark: Online estimates help establish a starting point before seeking professional valuations.

While useful, online tools cannot always account for recent renovations, unique property features, or the overall condition of a home.

Estate Agents

Local estate agents provide valuable insights because they actively monitor buyer behaviour and property trends within specific neighbourhoods. Their experience allows them to assess factors that automated systems may overlook.

- Local knowledge: Agents understand which features buyers currently value most in a particular area.

- Current demand insights: They can explain how market conditions are influencing asking prices and sales activity.

- Comparable properties: Agents often have access to recent sales information that may not yet be reflected in public databases.

Obtaining valuations from more than one estate agent can help identify a realistic pricing range rather than relying on a single opinion.

Surveyors

A qualified surveyor can provide one of the most detailed and objective property valuations available. Their assessments are based on professional standards and thorough property inspections.

- Independent assessment: Surveyors provide unbiased valuations based on factual property characteristics.

- Detailed analysis: Structural condition, location, property size, and market evidence are carefully evaluated.

- Professional reporting: Formal valuation reports can be useful for legal, financial, or lending purposes.

Surveyor valuations are often considered the most reliable option when accuracy is particularly important.

Research Recent Local Property Sales

Understanding what similar properties have recently sold for can significantly improve the accuracy of your estimate. Recent sales data provides a real-world indication of what buyers are currently willing to pay rather than what sellers hope to achieve.

Reviewing Sold Prices

Looking at recently sold properties in your area helps establish realistic expectations about value.

- Comparable size: Focus on homes with a similar number of bedrooms, bathrooms, and overall floor area.

- Similar condition: Compare properties with a comparable level of maintenance and upgrades.

- Nearby locations: Properties within the same neighbourhood often provide the most relevant benchmarks.

Sold prices generally offer a more accurate indication of market value than advertised asking prices.

Understanding Local Market Activity

Property values are influenced by local conditions that may vary significantly between regions and even individual neighbourhoods.

- Buyer demand: Areas with strong demand often experience faster price growth.

- Housing supply: Limited availability of similar properties can increase values.

- Community developments: New schools, transport links, and infrastructure projects can positively affect property prices.

Monitoring local market activity helps ensure your estimate reflects current conditions rather than outdated trends.

Keep Property Information Up To Date

Accurate property data is essential when estimating a home’s value. Missing or outdated information can result in valuations that fail to reflect the true worth of the property.

Renovations

Home improvements often increase property value when completed to a high standard and aligned with buyer expectations.

- Modern kitchens: Updated kitchens are frequently viewed as desirable by prospective buyers.

- Bathroom upgrades: Contemporary bathrooms can enhance both functionality and appeal.

- Interior improvements: Flooring, lighting, and decorative updates may improve market perception.

When obtaining valuations, make sure any recent improvements are clearly documented and communicated.

Extensions

Additional living space can significantly influence a property’s market value.

- Extra bedrooms: Additional bedrooms often increase a home’s appeal to families.

- Expanded living areas: Larger open-plan spaces can attract more buyers.

- Functional layouts: Well-designed extensions that improve usability are generally viewed positively.

Valuation tools and professionals should be informed of any completed extensions to ensure accurate assessments.

Energy Efficiency Improvements

Energy efficiency has become increasingly important to many UK buyers due to rising energy costs and environmental awareness.

- Improved EPC ratings: Higher energy performance ratings can increase buyer interest.

- Modern insulation: Effective insulation contributes to lower running costs.

- Energy-efficient systems: Updated heating systems and efficient windows can improve marketability.

These improvements may not always be reflected in automated valuation systems, making it important to provide accurate information during the valuation process.

Seek Professional Advice When Needed

While online estimates and local research can be helpful, there are situations where professional guidance becomes especially important. Expert advice can reduce uncertainty and provide greater confidence when making significant financial decisions.

Complex Properties

Some homes have characteristics that make automated valuations less reliable.

- Unique architecture: Distinctive designs can be difficult to compare with standard properties.

- Rural locations: Limited sales data may reduce estimate accuracy.

- Mixed-use properties: Homes with commercial elements often require specialist assessment.

Professional valuers can account for these complexities more effectively than automated tools.

High-Value Homes

Luxury and high-value properties often require a more detailed valuation process because there may be fewer comparable sales available.

- Specialised features: Premium finishes and bespoke designs can influence value significantly.

- Limited comparables: Fewer similar sales may exist within the local market.

- Market sensitivity: High-value properties can respond differently to changing market conditions.

Expert advice helps ensure these unique factors are properly considered.

Legal Or Financial Decisions

Certain situations require a formal and professionally prepared valuation rather than an informal estimate.

- Mortgage applications: Lenders often require independent property valuations.

- Inheritance matters: Accurate valuations may be necessary for estate planning and tax purposes.

- Divorce settlements: Property values often play a key role in financial negotiations.

- Investment planning: Reliable valuations support informed property investment decisions.

A qualified professional can provide documentation and evidence that may be required for legal or financial purposes.

Obtaining the most accurate house price estimate requires a combination of reliable data, local market knowledge, and professional insight. By comparing multiple valuation sources, reviewing recent property sales, keeping property details current, and seeking expert advice when appropriate, homeowners can gain a clearer and more realistic understanding of their property’s true market value.

House Price Estimates Across Different UK Regions

House price estimates across the UK can vary widely because each region has its own housing demand, local economy, buyer behaviour, property supply, and lifestyle appeal. A house price estimate UK search should never be treated as one-size-fits-all, because the same type of property can attract very different valuations depending on where it is located. Understanding these regional differences helps homeowners, buyers, and investors make more realistic decisions when assessing property value.

London Property Valuations

London remains one of the most complex property markets in the UK because prices can shift significantly from one borough to another. A flat in a well-connected central location may be valued very differently from a similar-sized property in an outer borough, even when the property type looks almost the same on paper.

Several location-based factors influence London property valuations, including transport access, school catchment areas, employment hubs, regeneration projects, and nearby amenities. Properties close to Underground stations, major business districts, parks, or highly rated schools often attract stronger buyer demand. However, affordability pressures, mortgage rates, and changing work patterns can also affect how quickly homes sell and what buyers are willing to pay.

- Transport Links: Homes near Underground, Overground, Elizabeth Line, or major rail stations often receive stronger interest because commuting convenience remains a major buyer priority.

- Borough Differences: Prime areas such as Kensington, Chelsea, Westminster, and parts of Camden often sit in a different pricing bracket from outer-London locations.

- Property Type: Flats, period homes, new-build apartments, and terraced houses can perform differently depending on lease length, service charges, outdoor space, and local demand.

- Buyer Demand: International buyers, professionals, families, and investors all influence different parts of the London market in different ways.

For anyone reviewing a house price estimate in London, it is important to compare recent sold prices within the same postcode or nearby streets rather than relying only on wider city averages.

South East England Market Trends

The South East often benefits from strong demand because it offers access to London while providing more space, commuter towns, coastal areas, and family-friendly communities. Property values in this region are heavily influenced by transport connections, local schools, employment opportunities, and quality-of-life factors.

Popular towns with fast rail links to London can command higher prices, especially when buyers want larger homes without fully leaving the commuter belt. Areas in Surrey, Kent, Berkshire, Hampshire, Oxfordshire, and Sussex often attract families, professionals, and downsizers, but values still vary greatly depending on the exact town, neighbourhood, and property condition.

- Commuter Access: Homes near reliable train routes into London often receive higher valuations because they appeal to professionals balancing work and lifestyle needs.

- School Catchments: Family buyers may pay more for properties close to well-regarded schools, making catchment areas an important valuation factor.

- Lifestyle Appeal: Villages, coastal towns, countryside locations, and market towns can attract strong demand when they offer space, character, and local amenities.

- Affordability Shifts: Some buyers move from London to the South East for more space, but higher mortgage costs can affect how much they are prepared to offer.

A house price estimate in the South East should consider both local sold-price data and buyer motivation. Two homes with the same number of bedrooms may have very different values if one is close to a mainline station and the other is in a less-connected location.

Northern England Property Estimates

Northern England includes a wide range of property markets, from major cities such as Manchester, Leeds, Liverpool, Sheffield, and Newcastle to rural towns, coastal areas, and smaller communities. Because of this variety, house price estimates in the North should be based on local evidence rather than broad regional assumptions.

In many northern cities, regeneration, student demand, employment growth, and transport improvements have influenced property values. City-centre apartments may appeal to professionals and investors, while suburban homes may attract families looking for more space and better affordability compared with the South.

- City Growth: Manchester, Leeds, Liverpool, and Newcastle have seen strong interest in areas linked to jobs, universities, retail, and regeneration.

- Affordability: Many northern areas offer lower entry prices than London and the South East, which can attract first-time buyers and investors.

- Local Variation: Prices can change sharply between neighbouring towns depending on employment, transport, schools, and housing stock.

- Rental Demand: In university cities and employment hubs, rental demand can influence investor interest and local property values.

For a more accurate property estimate in Northern England, it helps to check recent sold prices for similar homes within the same neighbourhood. A regional average may give a broad guide, but it will not reflect street-level differences in demand, condition, and buyer appeal.

Scotland, Wales, and Northern Ireland Considerations

Scotland, Wales, and Northern Ireland each have distinct property systems, regional markets, and buyer expectations. This means a house price estimate UK tool may give a useful starting point, but local context remains essential when reviewing value in these areas.

In Scotland, the buying process differs from England and Wales, with Home Reports playing an important role in property transactions. In Wales, values can vary between city markets such as Cardiff and Swansea, coastal communities, rural areas, and commuter locations near the English border. In Northern Ireland, local economic conditions, housing supply, and area-specific demand can strongly influence valuations.

- Scotland: Home Reports provide important property information, including survey details and valuation guidance, which can help buyers understand the condition and value of a home.

- Wales: Property values differ widely between cities, valleys, coastal towns, and rural locations, so local-market comparisons are especially important.

- Northern Ireland: House prices can be influenced by employment centres, school access, transport routes, and supply levels in specific towns and neighbourhoods.

- Rural Areas: In less-populated locations, fewer comparable sales can make online estimates less reliable, especially for unique homes or larger plots.

When estimating property values in these parts of the UK, it is wise to combine online valuation tools with local estate-agent insight and recent comparable sales. This is especially important for rural properties, character homes, and areas with fewer recent transactions.

Regional differences play a major role in every house price estimate, so a realistic valuation should always consider local demand, recent sold prices, property type, condition, and area-specific buyer behaviour. By looking beyond national averages and focusing on local evidence, homeowners and buyers can make better-informed decisions with greater confidence.

If you want a clearer understanding of what your property could be worth in today’s market, take the next step by exploring trusted valuation resources and expert guidance tailored to your situation. Accurate property insights can help you make more confident decisions whether you are selling, buying, remortgaging, or planning for the future, and our comprehensive resources are designed to give you the reliable information you need to move forward with confidence.

References

- UK House Price Index

https://www.gov.uk/government/statistics/uk-house-price-index-england-june-2025 - House Prices

https://www.ons.gov.uk/economy/inflationandpriceindices/datasets/housepriceindexmonthlyquarterlytables1to19 - Sold House Prices

https://www.rightmove.co.uk/house-prices.html - Property Valuation Guide

https://hoa.org.uk/advice/guides-for-homeowners/i-am-selling/how-much-is-my-house-worth/ - House Price Statistics for Small Areas

https://www.gov.uk/government/statistical-data-sets/price-paid-data-downloads - UK Residential Property Market Analysis

https://www.savills.co.uk/research_articles/229130/market-forecasts.aspx

FAQs: About House Price Estimate In UK

What is a house price estimate UK?

A house price estimate UK is an approximate valuation of a property based on location, size, condition, recent sold prices, and market trends. It helps homeowners, buyers, and investors understand a property’s likely market value.

How accurate are online house price estimates?

Online estimates can be useful as a starting point, but they are not always exact. Accuracy depends on the quality of local sales data, property details, and whether the home has unique features or recent improvements.

What factors affect a house price estimate?

Key factors include location, property size, number of bedrooms, condition, garden space, parking, transport links, schools, local demand, and recent nearby sales. Market conditions also play a major role.

Can I get a free house price estimate in the UK?

Yes, many online valuation tools and estate agents offer free house price estimates. However, a free estimate should usually be compared with other sources for a more balanced view.

Is a house price estimate the same as a property valuation?

No, a house price estimate is usually an informal guide, while a formal valuation may be completed by a surveyor, lender, or qualified professional. Formal valuations are often needed for mortgages, legal matters, or financial decisions.

How often does my house price change?

House prices can change regularly depending on buyer demand, interest rates, local sales, property condition, and wider economic trends. In active markets, values may shift within weeks or months.

What is the best way to estimate my house value?

The best approach is to compare online tools, recent sold prices, local estate agent advice, and professional valuations when needed. Using several sources gives a more reliable estimate than relying on one figure.

Do renovations increase a house price estimate?

Renovations can increase value if they improve usability, condition, energy efficiency, or living space. Kitchens, bathrooms, extensions, loft conversions, and kerb appeal improvements often influence buyer interest.

Why do different valuation tools show different prices?

Different tools use different data sources, formulas, update schedules, and assumptions. Some may rely heavily on nearby sold prices, while others may not fully account for renovations, condition, or unique property features.

Should I speak to an estate agent before selling?

Yes, speaking to a local estate agent can help you understand current buyer demand, realistic asking prices, and how your property compares with similar homes nearby. This can make your pricing strategy more accurate.

Conclusion

Getting a reliable house price estimate in the UK starts with understanding how property valuations work and why no single figure should be treated as final on its own. Online valuation tools can give a useful starting point, especially when they use recently sold price data and local market trends, but they may not fully account for your home’s condition, improvements, layout, kerb appeal, or unique location factors. For the most accurate view, it is best to compare multiple valuation methods, including online estimates, recent nearby property sales, local market research, estate-agent advice, and, where needed, a professional valuation from a qualified surveyor. This balanced approach helps you make better-informed decisions, whether you are buying, selling, remortgaging, investing, or simply reviewing your property’s current market value. If you need a more precise assessment before making a financial decision, speak with a local property expert or arrange a professional valuation so you can move forward with clearer expectations and greater confidence.