Estimate Cost To Rebuild House UK: Complete Guide

Welcome to our complete guide on how to estimate the cost to rebuild a house in the UK. Whether you are reviewing your home insurance, planning a major renovation, assessing the impact of property damage, or simply wanting a clearer understanding of rebuilding expenses, knowing your property’s rebuild cost is essential for protecting your investment and avoiding costly mistakes. Many homeowners mistakenly assume that a home’s market value reflects its rebuild cost, but the two figures can differ significantly. In this guide, you will learn what rebuild costs include, the factors that influence pricing, average rebuilding costs across the UK, and practical methods for calculating an accurate estimate. By understanding these key considerations, you can make informed financial decisions, maintain appropriate insurance cover, and confidently plan for future property projects.

To estimate the cost to rebuild a house in the UK, multiply the property’s total floor area by the average rebuild cost per square metre, then add professional fees, demolition costs, and site-specific expenses. Most UK rebuild costs vary based on location, property type, materials, and construction complexity.

What Does “Rebuild Cost” Mean?

Understanding rebuild cost is essential for homeowners, property investors, and anyone responsible for insuring a property. While many people focus on what a house is worth on the open market, rebuild cost refers to something entirely different. It represents the amount it would cost to reconstruct your home from the ground up if it were completely destroyed. This figure includes labour, materials, professional fees, site clearance, and other construction-related expenses. Knowing your property’s rebuild cost helps ensure you have the right level of insurance cover and can make informed financial decisions about your home.

Rebuild Cost vs Market Value

One of the most common areas of confusion for homeowners is the difference between rebuild cost and market value. Although the two figures are related to the same property, they are calculated for very different purposes.

Market value is the amount a buyer would be willing to pay for a property in its current location and condition. This figure is influenced by factors such as local demand, school catchment areas, transport links, and overall property market conditions.

Rebuild cost, on the other hand, focuses solely on the expense of reconstructing the physical structure. It does not take the value of the land into account and is based on current construction costs.

For example, a property located in a highly desirable area may have a market value significantly higher than its rebuild cost because much of its value comes from the land and location rather than the building itself.

Some common misconceptions include:

- Assuming insurance should match market value: Many homeowners believe their insurance cover should equal the property’s selling price, which can result in paying for more coverage than necessary.

- Believing rebuild cost never changes: Construction costs can fluctuate due to labour shortages, material prices, and inflation, meaning rebuild costs should be reviewed regularly.

- Thinking online property valuations provide rebuild figures: Property valuation tools generally estimate market value rather than the actual cost of rebuilding the home.

Understanding this distinction is important because using the wrong figure can lead to inaccurate insurance coverage and financial planning mistakes.

Why Rebuild Cost Matters

Rebuild cost is more than just a number for insurance paperwork. It plays a significant role in protecting your finances and helping you make informed decisions about your property.

Home Insurance Requirements

Most buildings insurance policies are based on a property’s rebuild cost rather than its market value. Insurers use this figure to determine the amount required to restore the property if it suffers severe damage from events such as fire, flooding, storms, or structural failure.

If a homeowner underestimates the rebuild cost, they risk being underinsured. This means the insurance payout may not fully cover the cost of reconstruction. Overestimating the figure can also result in unnecessarily high premiums.

A realistic rebuild estimate helps ensure the property is protected without paying for more coverage than needed.

Financial Planning and Budgeting

Knowing your rebuild cost can provide valuable insight when planning future property-related expenses. Whether you are considering improvements, refinancing, or long-term maintenance, understanding construction costs gives you a more accurate picture of your property’s financial requirements.

A rebuild assessment can also help homeowners prepare for unexpected events by understanding the true cost of replacing major structural elements if damage occurs.

Property Investment Decisions

For property investors, rebuild cost can be a useful metric when evaluating risk and potential returns. Investors often compare purchase prices, renovation budgets, insurance requirements, and projected expenses when assessing an opportunity.

Understanding rebuild costs may help identify properties that require higher insurance coverage, specialist construction methods, or additional contingency funding. This information supports more informed investment decisions and better risk management.

When You May Need a Rebuild Cost Estimate

Many homeowners only think about rebuild costs when renewing their insurance policy. However, there are several situations where obtaining an updated estimate is beneficial.

Insurance Renewals

Insurance providers often recommend reviewing rebuild costs periodically to ensure coverage remains accurate. Construction costs can change significantly over time, particularly during periods of rising material prices or labour shortages.

An updated rebuild estimate can help ensure your policy reflects current rebuilding expenses and reduces the risk of underinsurance.

Property Extensions and Major Renovations

Any significant change to your property can affect its rebuild cost. Extensions, loft conversions, structural alterations, and major renovations increase the amount of work and materials required to reconstruct the property.

Projects that may impact rebuild cost include:

- Home extensions: Additional living space increases total floor area and construction requirements.

- Loft conversions: Structural modifications and new rooms can raise rebuilding expenses.

- Kitchen renovations: High-specification finishes and custom installations may increase replacement costs.

- Property reconfigurations: Changes to layouts and supporting structures can affect reconstruction complexity.

After completing major works, it is wise to review your rebuild cost estimate and update your insurance provider accordingly.

Total Loss Scenarios After Disasters

While no homeowner likes to think about worst-case scenarios, severe events can result in extensive property damage or complete loss. Fires, floods, storms, subsidence, and other major incidents may require a property to be rebuilt entirely.

In these situations, an accurate rebuild cost becomes critical. It provides the financial foundation for restoring the home and helps ensure sufficient funds are available to cover demolition, site clearance, rebuilding, professional services, and compliance with current building regulations.

Being prepared before a disaster occurs can help reduce stress, minimise financial uncertainty, and support a smoother recovery process.

Average Cost To Rebuild A House In The UK

Understanding the average cost to rebuild a house in the UK is essential for homeowners, property investors, and anyone reviewing their home insurance coverage. Rebuild costs represent the amount required to reconstruct a property from the ground up if it is completely destroyed. This figure can vary significantly depending on the property’s size, location, construction materials, design complexity, and current market conditions. Having a realistic rebuild estimate helps ensure adequate insurance protection and provides a clearer understanding of potential construction expenses.

Typical Rebuild Costs Per Square Metre

One of the most common methods used to estimate the cost to rebuild a house in the UK is by calculating the average rebuild cost per square metre. While this approach provides a useful starting point, actual costs can vary based on several factors unique to each property.

Average Rebuild Cost Ranges

For many standard residential properties, rebuild costs are often calculated using a cost-per-square-metre basis. The average cost typically falls within a broad range because labour rates, material prices, and construction standards differ throughout the country.

Several factors influence these costs, including:

- Property Size: Larger homes generally require more materials, labour, and time to complete.

- Construction Quality: Premium finishes and specialist materials can significantly increase rebuilding expenses.

- Site Conditions: Challenging ground conditions or difficult access can add to construction costs.

- Professional Services: Architectural, surveying, and engineering fees often form part of the overall rebuild budget.

Standard Homes Vs Premium Properties

The quality and complexity of a property’s design play a major role in determining rebuild costs. Standard homes are usually built using conventional construction methods and readily available materials, making them more affordable to rebuild.

Premium properties often cost considerably more due to features such as:

- Custom Designs: Bespoke layouts and architectural details require additional planning and labour.

- High-End Materials: Premium stonework, specialist roofing, and luxury interior finishes increase material costs.

- Complex Construction: Unique structural features may require specialist trades and engineering expertise.

- Enhanced Specifications: Smart home systems, custom joinery, and luxury fixtures contribute to higher rebuilding expenses.

Regional Variations Across The UK

Location remains one of the biggest influences on rebuilding costs. Labour availability, contractor demand, and local construction markets can create significant pricing differences between regions.

For example:

- London And The South East: Generally experience higher labour and material costs due to strong demand and higher operating expenses.

- Major Cities: Urban areas often have increased construction costs because of site restrictions and logistical challenges.

- Rural Areas: Costs may vary depending on material transportation and the availability of skilled tradespeople.

- Scotland, Wales, And Northern Ireland: Regional market conditions can affect both labour rates and material pricing.

Rebuild Costs By Property Type

Different property types have distinct rebuilding requirements. The structure, size, layout, and construction methods all influence the overall cost of rebuilding.

Detached Houses

Detached houses are typically among the most expensive residential properties to rebuild because they have four external walls, larger roof structures, and more extensive foundations compared to attached properties. Larger detached homes may also feature garages, outbuildings, and landscaping elements that increase rebuilding costs.

Semi-Detached Homes

Semi-detached properties generally cost less to rebuild than detached homes because they share one wall with a neighbouring property. However, factors such as extensions, premium finishes, and structural complexity can still affect the final rebuild estimate.

Terraced Houses

Terraced houses often have lower rebuild costs due to their shared walls and more compact design. Despite this, rebuild expenses can increase if the property has undergone significant alterations or contains specialist architectural features.

Bungalows

Bungalows can sometimes surprise homeowners when it comes to rebuild costs. Although they have fewer storeys, they often require larger roof structures and more extensive foundations because all living space is located on a single level. This can result in higher construction costs per square metre compared to some two-storey homes.

Period And Listed Properties

Period homes and listed buildings are often the most expensive properties to rebuild. These properties may require specialist materials, traditional construction methods, and highly skilled craftspeople to preserve their historic character.

Additional cost factors may include:

- Heritage Requirements: Compliance with conservation regulations.

- Specialist Materials: Matching original stone, brickwork, or timber.

- Traditional Craftsmanship: Skilled restoration work often takes longer and costs more.

- Regulatory Approvals: Additional planning and heritage permissions may be required.

Sample Rebuild Cost Examples

Looking at practical examples can help homeowners understand how rebuild costs may vary between different property sizes and types. While actual costs depend on individual circumstances, these examples illustrate the factors that commonly influence rebuilding budgets.

Small Family Home

A small family home with a straightforward layout and standard construction materials will generally have a lower rebuild cost than larger or more complex properties. Costs are typically driven by floor area, local labour rates, and the quality of finishes selected during reconstruction.

Medium-Sized Detached Property

A medium-sized detached property often falls into the mid-range of rebuilding costs. These homes usually involve larger foundations, more extensive roofing systems, and increased material requirements. Features such as integrated garages, extensions, or upgraded finishes can further increase the overall budget.

Larger Executive Home

Executive homes typically involve higher rebuild costs due to their size, architectural complexity, and premium specifications. Large floor areas, bespoke design features, luxury finishes, and specialist construction methods all contribute to increased expenses. These properties often require detailed planning and a greater level of project management throughout the rebuilding process.

Estimating the cost to rebuild a house in the UK requires more than simply applying an average figure. Property size, location, design complexity, and construction quality all play important roles in determining the final cost. By understanding these factors and seeking professional guidance when necessary, homeowners can make informed decisions and ensure their insurance coverage accurately reflects the true cost of rebuilding their property.

Key Factors That Affect House Rebuild Costs

When estimating the cost to rebuild a house in the UK, it is important to understand that no two projects are exactly the same. Rebuild costs can vary significantly depending on the size of the property, where it is located, the materials used, and the complexity of the design. Even factors such as site access and local regulations can influence the final figure. Understanding these variables can help homeowners create a more accurate budget, avoid unexpected expenses, and ensure their insurance coverage reflects the true cost of rebuilding.

Property Size and Floor Area

One of the most important factors affecting house rebuild costs is the total floor area of the property. In most cases, rebuild estimates are calculated using a cost-per-square-metre approach, making the size of the home a primary driver of overall expenses.

Larger homes require more materials, labour, and construction time, which naturally increases costs. However, the relationship between size and cost is not always straightforward. A compact home with premium finishes and complex features may cost more per square metre than a larger, more standard property.

Key considerations include:

- Total Floor Space: Larger properties require more structural materials, roofing, insulation, and internal finishes.

- Number of Rooms: Additional bathrooms, kitchens, and utility spaces increase installation and finishing costs.

- Internal Layout: Open-plan designs, vaulted ceilings, and large living areas may require specialised construction methods.

- Future Adaptability: Homes designed with flexible living spaces may involve additional structural work that affects rebuilding expenses.

Accurately measuring the gross internal floor area is one of the first steps in creating a reliable rebuild cost estimate.

Location and Regional Labour Rates

The location of a property plays a major role in determining rebuild costs across the UK. Labour rates, material transportation expenses, and local demand for skilled trades can vary considerably between regions.

Properties located in London and the South East typically attract higher rebuilding costs due to increased labour rates, higher operating expenses, and strong demand within the construction industry. In contrast, some regions in Northern England, Wales, Scotland, and Northern Ireland may benefit from lower labour costs, although local market conditions still influence pricing.

Several location-based factors can affect rebuild costs:

- Labour Availability: Areas with shortages of skilled tradespeople often experience higher labour charges.

- Material Transport Costs: Remote locations may incur additional delivery expenses for building materials.

- Urban Construction Challenges: City-centre sites can involve restricted working hours, parking limitations, and logistical complications.

- Regional Demand: Areas experiencing high levels of development may see increased construction costs due to competition for resources.

Even homes with similar designs and sizes can have significantly different rebuild costs depending on their location.

Construction Materials

The materials chosen for a property have a direct impact on both rebuilding costs and long-term maintenance requirements. Standard materials generally offer lower rebuild costs, while premium or specialist materials can increase the overall budget considerably.

Brick remains one of the most common construction materials in the UK due to its durability and relatively predictable cost. Timber-frame construction is also popular and can sometimes reduce build times, while natural stone properties often require specialist skills and materials that increase rebuilding expenses.

Material choices that commonly influence costs include:

- Brick Construction: Widely used and generally cost-effective for many residential properties.

- Timber-Frame Systems: Often provide faster construction times but may require specialist design and installation.

- Natural Stone: Creates a distinctive appearance but typically involves higher labour and material costs.

- Specialist Materials: Heritage materials, bespoke finishes, and imported products can significantly increase rebuilding expenses.

It is also worth considering long-term ownership costs. Higher-quality materials may require less maintenance and provide greater durability over time, making them a worthwhile investment in some situations.

Design Complexity

The complexity of a property’s design can have a substantial effect on rebuild costs. While straightforward house designs are generally easier and less expensive to reconstruct, properties with unique architectural features often require additional planning, specialist trades, and bespoke materials.

Custom-built homes frequently involve construction details that are not found in standard housing developments. These features can increase both labour requirements and project timelines.

Common design-related cost factors include:

- Architectural Features: Curved walls, large glazed areas, and bespoke detailing often require specialist construction techniques.

- Multiple Storeys: Additional floors increase structural requirements and construction complexity.

- Complex Roof Designs: Dormers, gables, and unusual roof structures typically require more labour and materials.

- Open-Plan Spaces: Large unsupported spans may require steel beams and structural engineering input.

The more unique a property is, the more likely it is that rebuilding will require specialist expertise and higher project costs.

Access and Site Conditions

Site-specific conditions can significantly affect the cost of rebuilding a house, regardless of its size or design. Construction teams need safe and practical access to deliver materials, operate equipment, and complete the work efficiently.

Restricted access can increase labour requirements and slow down progress, while challenging ground conditions may require additional engineering solutions before construction can begin.

Important site considerations include:

- Restricted Access: Narrow driveways, steep sites, or limited vehicle access can increase labour and transportation costs.

- Demolition Requirements: Existing structures may need to be safely demolished and removed before rebuilding begins.

- Ground Conditions: Poor soil quality or unstable ground may require specialist foundation systems.

- Drainage Challenges: Water management issues can increase excavation and foundation costs.

Site investigations and professional surveys are often essential for identifying potential issues before construction starts, helping to reduce the risk of unexpected expenses later in the project.

Building Regulations and Planning Requirements

Every rebuild project must comply with current building regulations, even when replacing an existing structure. These regulations are designed to ensure that properties meet modern standards for safety, energy efficiency, accessibility, and structural performance.

Depending on the scope of the rebuild, homeowners may also need planning permission, building control inspections, and professional design services. These requirements add costs that should be included in any rebuild estimate.

Typical compliance-related expenses include:

- Building Regulation Compliance: Meeting current standards for insulation, fire safety, ventilation, and structural performance.

- Planning Permission Fees: Required for certain rebuild projects, particularly where design changes are proposed.

- Structural Engineering Services: Necessary for foundation design, load calculations, and structural assessments.

- Professional Consultancy Fees: Architects, surveyors, and project managers often play an important role in complex rebuild projects.

Failing to account for these costs can lead to an underestimate of the true rebuild value of a property. Including professional and regulatory expenses from the outset helps create a more realistic budget and supports a smoother construction process.

Understanding the factors that influence house rebuild costs allows homeowners to make informed decisions when budgeting, obtaining insurance, or planning future projects. By considering property size, location, materials, design complexity, site conditions, and regulatory requirements, it becomes much easier to develop a realistic estimate that reflects the true cost of rebuilding a home in the UK.

Additional Costs Homeowners Often Overlook

When estimating the cost to rebuild a house in the UK, many homeowners focus primarily on construction materials and labour. However, several additional expenses can significantly affect the overall budget. Overlooking these costs can lead to financial surprises during the rebuilding process and may result in insufficient insurance coverage. Understanding these often-forgotten expenses can help you create a more accurate rebuild estimate and make better-informed decisions when planning a project or reviewing your home insurance.

Demolition and Site Clearance

Before rebuilding can begin, any damaged or existing structures may need to be removed safely and efficiently. Demolition and site-clearance costs vary depending on the size of the property, the complexity of the work, and site accessibility.

A straightforward demolition project may involve removing a standard residential structure and clearing debris from the site. However, more complex projects can require specialist equipment, waste disposal services, and environmental assessments. If hazardous materials such as asbestos are present, removal must be completed by licensed professionals, which can increase costs considerably.

Factors that can influence demolition and site-clearance costs include:

- Property Size: Larger buildings generally require more labour, equipment, and disposal resources.

- Waste Removal: Construction waste must be transported and disposed of in accordance with environmental regulations.

- Hazardous Materials: Asbestos and other dangerous substances require specialist handling and removal.

- Site Access: Restricted-access sites may require additional equipment or manual labour.

Including demolition and clearance expenses in your rebuild estimate ensures you have a realistic understanding of the total project cost from the outset.

Professional Fees

Many homeowners underestimate the professional expertise required to complete a successful rebuild project. Professional fees can represent a significant portion of the overall budget, particularly for larger or more complex properties.

Architects

Architects help transform ideas into practical, compliant building designs. They prepare plans, coordinate with other professionals, and ensure the project meets planning and building regulation requirements. Their involvement can be particularly valuable for custom-designed homes or properties with unique architectural features.

Surveyors

Surveyors provide accurate property measurements, assess site conditions, and prepare rebuild valuations for insurance purposes. Their reports help ensure that estimates are based on reliable information rather than assumptions.

Structural Engineers

Structural engineers evaluate the safety and stability of the proposed structure. They design load-bearing elements, foundations, and structural systems that comply with current building standards. Their expertise is often essential for properties with complex layouts or challenging ground conditions.

Project Managers

A project manager oversees schedules, budgets, contractors, and communication throughout the rebuild. While hiring a project manager adds an upfront cost, effective project management can help prevent delays, reduce costly mistakes, and improve overall efficiency.

Common professional fees may include:

- Design Services: Architectural drawings, design revisions, and planning support.

- Surveying Costs: Site surveys, measured surveys, and rebuild valuations.

- Engineering Assessments: Structural calculations and technical reports.

- Project Oversight: Coordination of contractors, suppliers, and project timelines.

Planning Permission And Building Control Fees

Planning permission and building-control fees are important considerations when calculating rebuild costs. While some rebuild projects may qualify for simplified approval processes, many require formal applications and inspections.

Planning permission fees cover the review and assessment of proposed building works by the local planning authority. Building-control fees support inspections that verify compliance with safety, structural, and energy-efficiency standards throughout the construction process.

Typical costs can vary based on:

- Project Scope: Larger or more complex developments may require additional reviews.

- Local Authority Charges: Fees differ between councils and regions.

- Specialist Reports: Some projects require environmental, drainage, or heritage-related assessments.

- Inspection Requirements: Multiple site visits may be necessary during construction.

Failing to account for these expenses can lead to delays or unexpected budget increases later in the project.

Utility Connections And Infrastructure

Rebuilding a home often involves reconnecting or replacing essential services. Utility and infrastructure costs are frequently overlooked because they are not always visible during the initial planning stages.

Depending on the extent of the rebuild, connections may need to be upgraded to meet modern standards or relocated to accommodate the new design. These costs can vary significantly depending on the property’s location and existing infrastructure.

Key utility-related expenses include:

- Water Supply: Connection fees, pipe installation, and meter upgrades.

- Electricity Services: New cabling, upgraded supply capacity, and connection charges.

- Gas Connections: Installation, reconnection, and compliance testing.

- Drainage Systems: Repairs, upgrades, or new drainage infrastructure where required.

Properties in rural or remote locations may face higher connection costs due to increased installation distances and infrastructure requirements.

Landscaping And External Works

Many rebuild estimates focus solely on the house itself while overlooking the surrounding property. Once construction is complete, external areas often require significant restoration or replacement.

Reinstating outdoor spaces can improve functionality, appearance, and property value. Depending on the extent of the work, these costs can become a substantial part of the overall budget.

Driveways

Construction activity frequently damages existing driveways, pathways, and paved areas. Replacing these surfaces may require excavation, groundwork, drainage improvements, and resurfacing.

Fencing

Boundary fencing may need repair or complete replacement following demolition and rebuilding work. Material choice, fence height, and site conditions can all influence costs.

Garden Reinstatement

Heavy equipment and construction traffic often affect lawns, planting areas, and landscaping features. Reinstating gardens may involve new turf, planting, retaining walls, irrigation systems, and decorative elements.

Common external-work costs include:

- Surface Restoration: Driveways, patios, and pathways.

- Boundary Improvements: Fencing, gates, and retaining structures.

- Garden Recovery: Turf installation, planting, and landscape enhancements.

- Drainage Adjustments: Surface water management and site grading.

VAT And Tax Considerations

VAT can have a significant impact on rebuild costs, making it essential to understand how tax rules apply to your specific project. The amount of VAT payable depends on the nature of the rebuild and whether any exemptions or reliefs are available.

In many cases, construction services and building materials are subject to VAT. However, certain projects may qualify for reduced rates or specific tax relief schemes. Eligibility often depends on the type of property, the scope of work, and compliance with HMRC requirements.

Important VAT considerations include:

- Standard VAT Charges: Many construction-related goods and services are subject to VAT.

- Reduced Rates: Some qualifying projects may benefit from reduced VAT rates.

- Reclaim Opportunities: Certain self-build projects may allow eligible VAT recovery.

- Documentation Requirements: Accurate records are essential when applying for tax relief or refunds.

Because VAT rules can be complex and subject to change, homeowners should seek professional tax advice when preparing a rebuild budget to ensure all available reliefs and exemptions are considered.

When estimating the cost to rebuild a house in the UK, accounting for these additional expenses can make the difference between a realistic budget and an unexpected financial shortfall. By considering demolition, professional services, regulatory fees, utility connections, external works, and tax obligations from the beginning, homeowners can develop a more accurate rebuild estimate and avoid costly surprises throughout the project.

How To Estimate The Cost To Rebuild A House In The UK

Estimating the cost to rebuild a house in the UK involves more than applying a simple figure to your property’s size. A reliable rebuild estimate should account for construction costs, labour rates, professional fees, demolition expenses, and site-specific factors that could affect the overall project budget. Whether you are reviewing your home insurance coverage or planning a future rebuild, understanding the different methods available can help you arrive at a more accurate figure and avoid costly surprises.

Use a Cost Per Square Metre Calculation

One of the most common ways to estimate rebuild costs is by using a cost per square metre calculation. This method provides a useful starting point and is widely used by homeowners, insurers, and property professionals.

The process involves determining the total floor area of your home and multiplying it by an estimated rebuild cost per square metre. The final figure can then be adjusted to reflect additional expenses such as demolition, professional services, and external works.

Step-by-Step Explanation

To calculate an estimated rebuild cost using this method:

- Measure The Floor Area: Calculate the total internal floor space of the property in square metres.

- Research Current Rebuild Rates: Identify average rebuild costs for similar properties in your region.

- Multiply Area By Cost: Multiply the property’s floor area by the chosen cost per square metre.

- Add Additional Expenses: Include demolition, site clearance, planning fees, and professional costs where applicable.

- Review Property Features: Consider factors such as premium finishes, unusual designs, or specialist materials that may increase costs.

This approach offers a practical estimate, but it should be viewed as a guide rather than a guaranteed rebuild figure.

Example Calculation

Imagine a detached house with a total floor area of 150 square metres. If the estimated rebuild cost is £2,000 per square metre, the basic rebuilding cost would be:

150m² × £2,000 = £300,000

If professional fees, demolition costs, and external works add an additional £30,000, the estimated total rebuild cost would be approximately £330,000.

While this example is simplified, it demonstrates how quickly costs can increase once additional project requirements are considered.

Use Rebuild Cost Calculators

Online rebuild cost calculators have become a popular tool for homeowners seeking a quick estimate. Many insurance providers and property organisations offer calculators designed to generate an approximate rebuilding value based on information about the property.

These tools can be useful during the early stages of research, especially when a professional assessment has not yet been arranged.

Benefits and Limitations

Rebuild calculators offer several advantages, but they also have limitations that homeowners should understand.

- Benefit: Provide a fast estimate without requiring professional assistance.

- Benefit: Help homeowners identify whether their current insurance coverage may be too high or too low.

- Benefit: Offer a useful starting point for budgeting and financial planning.

- Limitation: May not account for unique architectural features or specialist materials.

- Limitation: Often rely on standardised assumptions that may not reflect local construction conditions.

- Limitation: Cannot fully assess site-specific challenges such as difficult access or unusual ground conditions.

Because every property is different, rebuild calculators should be treated as an initial guide rather than a definitive valuation.

When Online Tools Are Useful

Online calculators are particularly useful when:

- Reviewing Insurance Coverage: They can provide a quick benchmark before renewing a policy.

- Planning Property Improvements: Homeowners can estimate how extensions or upgrades may affect rebuild costs.

- Comparing Property Options: Buyers can gain a general understanding of rebuilding expenses when evaluating different homes.

- Conducting Preliminary Research: They help establish realistic expectations before seeking professional advice.

For standard residential properties, a calculator may provide a reasonably accurate starting point. However, more complex homes often require expert evaluation.

Obtain a Professional Rebuild Assessment

For the most reliable estimate, many homeowners choose to obtain a professional rebuild assessment. This option provides a detailed evaluation that considers the unique characteristics of the property and current construction market conditions.

Professional assessments are particularly valuable for larger homes, high-value properties, listed buildings, and homes with non-standard construction methods.

Chartered Surveyors

Chartered surveyors have the expertise to assess a property’s rebuilding requirements and provide a detailed valuation based on recognised industry standards.

During an assessment, a surveyor may evaluate:

- Building Size: Total floor area and structural layout.

- Construction Type: Materials used throughout the property.

- Property Features: Special architectural details or custom-built elements.

- Site Conditions: Access restrictions, location, and ground conditions.

- Current Construction Costs: Local labour and material pricing.

A professionally prepared report often provides greater confidence than relying solely on online tools or generic estimates.

Insurance Rebuild Valuations

Insurance rebuild valuations are specifically designed to help homeowners determine the level of cover required to fully rebuild their property after a major loss.

These assessments typically include:

- Demolition Costs: Removal of damaged structures.

- Reconstruction Costs: Labour and material expenses.

- Professional Fees: Architectural, surveying, and engineering services.

- Regulatory Costs: Building control and compliance requirements.

An accurate insurance rebuild valuation helps reduce the risk of underinsurance, which can leave homeowners responsible for unexpected costs following a claim.

Compare Multiple Estimates

Rebuild costs can vary significantly depending on who prepares the estimate and the assumptions used during the calculation process. Comparing multiple estimates provides a broader understanding of likely costs and helps identify inconsistencies that may require further investigation.

Rather than accepting the first figure received, it is often worth reviewing several sources before making decisions about insurance or budgeting.

Why Estimates Can Vary

Several factors contribute to differences between rebuild estimates:

- Regional Pricing: Labour and material costs vary throughout the UK.

- Methodology Used: Different providers may use different calculation models.

- Property Complexity: Unique design features can be interpreted differently.

- Market Conditions: Construction costs can change due to inflation and supply issues.

- Included Costs: Some estimates include professional fees and demolition costs, while others may not.

Understanding these differences can prevent confusion when comparing results.

What to Look for When Comparing Figures

When reviewing multiple rebuild estimates, focus on more than the final number.

Consider:

- Scope Of Costs Included: Check whether demolition, fees, and external works are covered.

- Date Of Assessment: Older estimates may not reflect current market conditions.

- Level Of Detail: Detailed reports often provide greater accuracy and transparency.

- Property Assumptions: Ensure the information used is accurate and up to date.

- Professional Credentials: Verify whether the estimate was prepared by a qualified expert.

Taking time to compare estimates carefully can help you make informed decisions and ensure your rebuild cost reflects the true expense of reconstructing your home.

Estimating the cost to rebuild a house in the UK is an important step for protecting your property and ensuring adequate insurance coverage. Whether you use a simple cost per square metre calculation, an online rebuild calculator, or a professional assessment, the most reliable results come from using accurate information and considering all potential costs. A well-informed estimate can provide peace of mind and help you prepare for future property decisions with confidence.

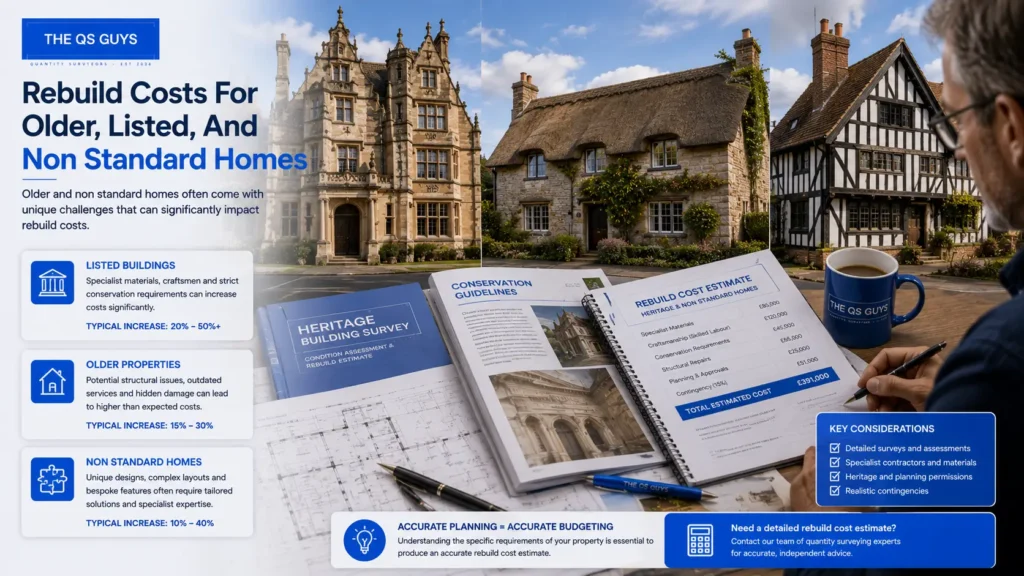

Rebuild Costs For Older, Listed, And Non-Standard Homes

Older, listed, and non-standard homes often cost more to rebuild than modern, standard properties because they are rarely simple like-for-like construction projects. The materials, design details, permissions, and specialist labour involved can all increase the final rebuild cost. For homeowners trying to estimate cost to rebuild house UK properties accurately, these details matter because a standard square-metre rate may not reflect the true cost of rebuilding a more complex home.

Why Heritage Properties Cost More

Heritage properties usually need more careful planning, skilled tradespeople, and specialist materials than newer homes. A modern house may be rebuilt using widely available bricks, blocks, roof tiles, and standard fittings, but an older home may need lime mortar, handmade bricks, natural stone, timber windows, slate roofing, or period-appropriate joinery.

These materials are often more expensive to source and slower to install. Labour costs can also be higher because the work may need craftspeople with experience in traditional building methods. For example, repairing or rebuilding a stone wall is not the same as building with modern concrete blocks. It takes time, knowledge, and attention to detail.

Heritage homes may also include features that are costly to replace, such as decorative plasterwork, sash windows, exposed beams, ornate fireplaces, or custom staircases. These details can make the property attractive and valuable, but they also make a rebuild estimate more complicated.

- Specialist materials: Older properties may require natural stone, lime-based mortar, handmade tiles, or traditional timber, which can cost more than standard materials.

- Skilled craftsmanship: Traditional building techniques often require experienced tradespeople, which can increase labour costs.

- Longer project times: Sourcing materials, matching original details, and completing careful restoration-style work can extend the build schedule.

Listed Building Considerations

Listed buildings come with extra responsibilities because their historic or architectural value is legally protected. If a listed home needs to be rebuilt or repaired after serious damage, the owner may not be free to choose cheaper materials or simpler construction methods. The work often needs to respect the original character of the building.

Conservation requirements can affect almost every part of the project. Windows, doors, walls, roof coverings, internal features, and external finishes may all need to match the original design. This can make a rebuild more expensive than a typical modern home project, especially when specialist reports or heritage consultants are required.

Regulatory approvals can also add time and cost. Depending on the property and the type of work required, homeowners may need listed building consent, planning permission, building control approval, and input from conservation officers. These steps are important, but they can make the rebuild process slower and more detailed.

- Conservation requirements: Work may need to preserve original materials, design features, and historic character.

- Regulatory approvals: Listed building consent and local authority approval may be needed before major work can begin.

- Professional input: Surveyors, architects, structural engineers, and heritage specialists may need to be involved to ensure the rebuild meets legal and conservation standards.

- Higher insurance risk: If the rebuild cost is underestimated, the insurance cover may not be enough to restore the property properly after major damage.

Non-Standard Construction Types

Non-standard homes can be harder to price because they do not follow typical modern-construction methods. This includes timber-framed homes, stone cottages, thatched properties, converted barns, eco homes, and architect-designed houses with unusual layouts or materials. These properties often need a more detailed rebuild valuation because average rebuild cost figures may be too broad.

Timber-framed homes can vary widely in rebuild cost depending on the frame type, age, condition, and finish. A modern timber-frame property may be straightforward to rebuild, while an older exposed-frame home may need specialist carpentry and careful structural work.

Stone cottages can also be more expensive than standard brick-built homes. Natural stone may need to be locally sourced or carefully matched to the existing building. Thick walls, uneven layouts, and older foundations can add further complexity.

Unique architectural properties may include large glass sections, bespoke steelwork, curved walls, unusual rooflines, custom interiors, or high-specification finishes. These features may not be covered properly by simple online rebuild calculators, so a professional assessment is usually the safer option.

- Timber-framed homes: Costs depend on whether the frame is modern, historic, exposed, structural, or decorative.

- Stone cottages: Rebuilding may require matched stone, specialist masonry, and careful work around older foundations.

- Unique architectural properties: Bespoke layouts, custom materials, and unusual structural details can increase design, labour, and replacement costs.

- Limited comparison data: Non-standard homes are harder to benchmark, so generic rebuild estimates can be unreliable.

For older, listed, and non-standard homes, the safest approach is to avoid relying only on broad online averages. A professional rebuild-cost assessment can help reflect the real materials, labour, permissions, and specialist work involved, giving homeowners a more reliable figure for insurance and long-term property planning.

How Inflation And Market Conditions Affect Rebuild Costs

When estimating the cost to rebuild a house in the UK, it is important to understand that rebuild costs are not fixed. Construction expenses can change significantly over time due to inflation, supply chain disruptions, labour availability, and broader economic conditions. Even if a rebuild estimate was accurate a few years ago, it may no longer reflect current market realities. Keeping up with these changes helps homeowners maintain adequate insurance coverage and make better-informed financial decisions.

Construction Material Price Changes

The cost of construction materials is one of the biggest factors influencing house rebuild costs. Materials such as timber, steel, concrete, bricks, roofing products, and insulation are subject to price fluctuations based on supply, demand, and global economic conditions. When material costs rise, the overall expense of rebuilding a property increases as well.

Supply Chain Impacts

Construction projects rely on a complex network of manufacturers, suppliers, transport providers, and distributors. When disruptions occur within this network, material shortages and higher prices often follow. Events such as transportation delays, manufacturing slowdowns, increased fuel costs, or international trade restrictions can affect the availability of essential building materials.

Some common supply chain challenges include:

- Transportation Delays: Longer delivery times can slow construction schedules and increase project costs.

- Material Shortages: Limited availability of key products can force builders to source more expensive alternatives.

- Import Costs: Increased shipping expenses and tariffs may raise the cost of imported materials.

- Supplier Capacity Issues: High demand can strain manufacturers and reduce stock availability.

These factors can have a direct impact on rebuild estimates, particularly during periods of market instability.

Volatile Material Markets

Material prices do not always increase steadily. Certain products experience rapid price changes depending on market demand and supply conditions. For example, timber and steel prices have experienced significant fluctuations in recent years due to changes in global demand, production levels, and economic uncertainty.

Property owners should be aware that:

- Commodity-Based Materials: Products such as steel, timber, and copper can experience substantial price swings.

- Energy Costs: Rising energy prices can increase manufacturing expenses, leading to higher material costs.

- Demand Surges: Increased construction activity can drive prices higher when supply struggles to keep pace.

- Economic Conditions: Inflation and market uncertainty can affect pricing across the construction sector.

Because of these variables, rebuild costs can change considerably within a relatively short period.

Labour Shortages and Demand

While material costs attract significant attention, labour expenses are equally important when estimating rebuild costs. The availability of skilled tradespeople plays a major role in determining the overall cost of construction work.

Skilled Trades Availability

The construction industry relies on experienced professionals, including bricklayers, carpenters, electricians, plumbers, roofers, and plasterers. When demand for these trades exceeds available supply, labour rates often increase.

Several factors contribute to labour shortages:

- High Construction Demand: More building projects can create competition for skilled workers.

- Workforce Ageing: Retirements within the industry can reduce the number of experienced tradespeople.

- Training Gaps: Fewer new workers entering certain trades can create long-term shortages.

- Regional Differences: Some parts of the UK experience greater labour shortages than others.

When skilled trades become harder to secure, contractors may charge higher rates, which can significantly affect house rebuild costs. In busy construction markets, labour shortages can also extend project timelines, adding further expense to a rebuild project.

Why Rebuild Costs Should Be Reviewed Regularly

Because construction costs are influenced by changing market conditions, homeowners should not assume that a rebuild valuation will remain accurate indefinitely. Regular reviews help ensure that insurance coverage and financial planning remain aligned with current rebuilding expenses.

Insurance Implications

One of the most important reasons to review rebuild costs is to avoid underinsurance. If a property’s rebuild cost has increased but the insurance policy has not been updated, the homeowner may not have sufficient cover to fully rebuild the property following a major loss.

Potential risks include:

- Underinsurance: The policy may not cover the full cost of rebuilding.

- Reduced Claims Settlements: Some insurers may apply proportional reductions when a property is significantly underinsured.

- Unexpected Out-of-Pocket Costs: Homeowners may need to fund part of the rebuilding work themselves.

- Financial Stress: Insufficient cover can create substantial financial challenges after a serious incident.

Regular reviews can help ensure that insurance protection remains appropriate as construction costs change.

Maintaining Accurate Valuations

An accurate rebuild valuation provides a reliable foundation for insurance decisions, financial planning, and property management. Rebuild costs can increase over time due to inflation, changes in building regulations, labour shortages, and rising material prices.

Homeowners should consider updating rebuild estimates when:

- Major Renovations Are Completed: Extensions and upgrades can significantly increase rebuild costs.

- Property Alterations Occur: Structural changes may affect valuation calculations.

- Insurance Policies Are Renewed: Reviewing costs during renewal periods helps maintain adequate cover.

- Market Conditions Change: Significant increases in construction costs may justify a reassessment.

Keeping rebuild valuations up to date allows homeowners to make informed decisions and reduces the risk of unexpected financial exposure if rebuilding becomes necessary.

Inflation and market conditions can have a significant impact on the true cost of rebuilding a property. By understanding how material prices, labour availability, and economic factors influence construction expenses, homeowners can make more accurate estimates, maintain appropriate insurance coverage, and better protect their investment over the long term.

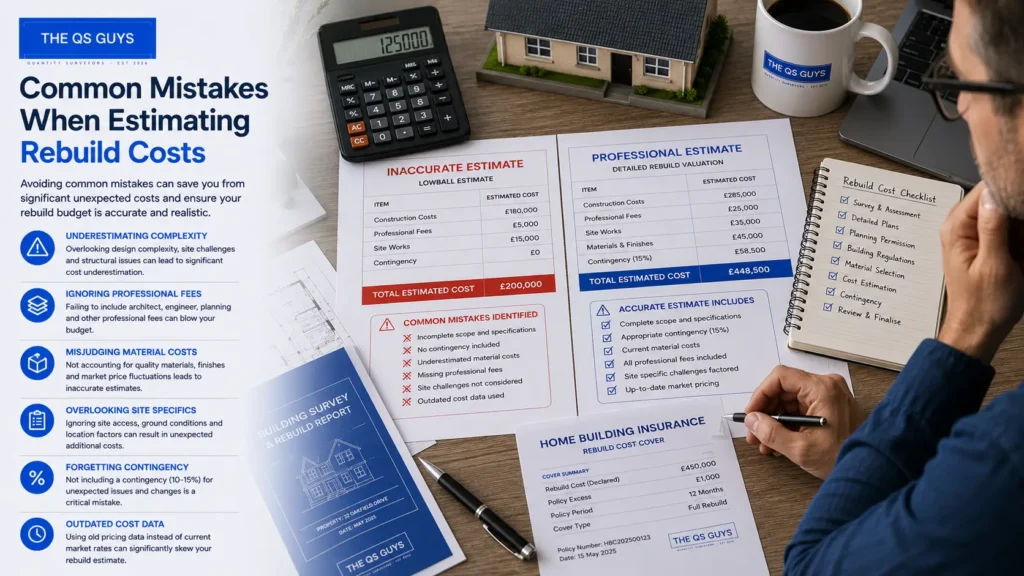

Common Mistakes When Estimating Rebuild Costs

Estimating rebuild costs can seem straightforward, but small assumptions often lead to inaccurate figures. For UK homeowners, the risk is not just budgeting incorrectly. A poor rebuild-cost estimate can also affect home-insurance cover, claims outcomes, and long-term financial planning.

Confusing Market Value With Rebuild Cost

One of the most common mistakes is assuming that a property’s market value is the same as its rebuild cost. Market value is based on what someone may pay for the home, including location, land value, local demand, nearby amenities, and wider property-market conditions. Rebuild cost is different because it focuses on the cost of reconstructing the building itself.

A house in a high-value area may have a market price far above its rebuild cost, while a rural or older property may cost more to rebuild than its sale price suggests. This is why using a recent estate agent valuation or online property estimate can lead to the wrong insurance figure.

- Market value: Reflects the property’s sale price, land value, location, and buyer demand.

- Rebuild cost: Covers demolition, labour, materials, professional fees, building-control costs, and the work needed to reconstruct the property.

- Insurance risk: If the rebuild-cost estimate is too low, the homeowner may be underinsured and may not receive enough to fully rebuild after major damage.

Underestimating Professional Fees

Many people focus only on bricks, timber, roofing, and labour when calculating the cost to rebuild a house in the UK. In reality, professional fees can make up a meaningful part of the total cost. These fees are often necessary because a rebuild usually involves planning, design, compliance, inspections, and technical oversight.

Depending on the property, homeowners may need an architect, structural engineer, quantity surveyor, project manager, party-wall surveyor, or planning consultant. These costs can vary depending on the complexity of the project, the location, and whether the building has unusual structural or heritage requirements.

- Architect fees: May be needed for drawings, design work, planning submissions, and construction-stage support.

- Structural-engineer fees: Often required when foundations, load-bearing walls, roof structures, or complex designs are involved.

- Surveyor costs: Help produce a more accurate rebuild valuation, especially for older, listed, or non-standard properties.

- Compliance fees: Building-control inspections, planning applications, and specialist reports can add to the total rebuild budget.

Ignoring Site-Specific Challenges

A rebuild estimate should never be based on floor area alone. Two homes with the same square metreage can have very different rebuild costs because of access, ground conditions, nearby structures, slope, drainage, and demolition requirements. These site-specific details often affect labour time, machinery access, safety planning, and foundation work.

For example, rebuilding a house on a tight urban plot may cost more because contractors have limited space for materials, skips, scaffolding, and equipment. A sloped site may need extra retaining work. Poor ground conditions may require deeper foundations or specialist engineering.

- Restricted access: Narrow roads, shared driveways, or limited parking can increase labour and delivery costs.

- Ground conditions: Clay soil, unstable ground, flood risk, or drainage problems can affect foundation design.

- Demolition work: Removing damaged structures safely can add significant cost before rebuilding even begins.

- Neighbouring properties: Terraced and semi-detached homes may require extra care, party-wall agreements, or temporary structural support.

Relying on Outdated Cost Data

Construction costs change over time, so using an old rebuild-cost estimate can create a serious gap between the insured amount and the actual cost of reconstruction. Labour rates, material prices, fuel costs, supply-chain issues, and regulatory changes can all affect the final rebuild figure.

This is especially important for homeowners who have not reviewed their insurance cover for several years. A rebuild estimate that was accurate five years ago may no longer reflect current UK construction costs. Even modest inflation can have a large impact when applied to a full-house rebuild.

- Material-price changes: Roofing, timber, steel, concrete, insulation, and glazing costs can shift with market conditions.

- Labour-rate increases: Skilled trades are a major part of rebuild pricing, and shortages can increase costs.

- Regulation updates: Changes to energy-efficiency standards, fire safety, and building regulations can affect the work required.

- Insurance accuracy: Regular reviews help reduce the risk of underinsurance and make the policy more reliable.

Failing to Allow for Contingencies

A rebuild project can uncover issues that are not obvious at the estimate stage. Hidden structural problems, drainage defects, foundation complications, asbestos, difficult demolition conditions, and planning delays can all add cost. Without a contingency allowance, the budget may become unrealistic very quickly.

A sensible rebuild-cost estimate should include a contingency amount to cover unexpected expenses. This is not padding the budget. It is a practical way to reflect the uncertainty that comes with construction work, especially after fire, flood, storm, subsidence, or major structural damage.

- Unexpected discoveries: Asbestos, unstable ground, damaged drainage, or hidden structural defects can increase costs.

- Project delays: Bad weather, planning issues, contractor availability, and supply delays can affect the final price.

- Specification changes: Upgrading materials or changing layouts during the project can raise the rebuild budget.

- Better planning: A contingency helps homeowners, insurers, and contractors work with a more realistic cost estimate.

A reliable rebuild-cost estimate should be based on current data, professional input, and the real conditions of the property, not guesswork. By avoiding these mistakes, homeowners can make better insurance decisions, reduce financial risk, and plan with more confidence.

Getting an accurate rebuild cost estimate can help you avoid underinsurance, unexpected expenses, and costly planning mistakes. If you want greater confidence in your property’s true rebuilding value, explore our expert resources and professional guidance to make informed decisions, protect your investment, and ensure your estimate reflects current UK construction costs and market conditions.

References

- ABI Rebuild Cost Calculator

https://www.abi.org.uk/products-and-issues/topics-and-issues/home-insurance/calculators/ - MoneySuperMarket Guide to House Rebuild Costs

https://www.moneysupermarket.com/home-insurance/rebuild-cost-calculator/ - Compare the Market Rebuild Cost Guide

https://www.comparethemarket.com/home-insurance/content/rebuild-cost-calculator/

FAQs: About Estimate Cost To Rebuild House In UK

How do I estimate the cost to rebuild a house in the UK?

The most common method is to multiply the property’s total floor area by the average rebuild cost per square metre and then add costs for demolition, professional fees, and site-specific requirements. For greater accuracy, consider obtaining a professional rebuild valuation from a qualified surveyor.

Is the rebuild cost of a house the same as its market value?

No, rebuild cost and market value are different. Market value reflects what a property could sell for, while rebuild cost covers the expense of reconstructing the building from scratch, including labour, materials, and associated fees.

What is included in a house rebuild cost estimate?

A rebuild estimate typically includes construction materials, labour, demolition, site clearance, professional fees, building regulation costs, and utility reconnections. Some estimates may also account for landscaping and external structures.

How much does it cost to rebuild a house per square metre in the UK?

The average rebuild cost per square metre varies depending on location, build quality, and property type. Standard homes generally cost less to rebuild than luxury or bespoke properties with premium materials and complex designs.

Why do insurance companies ask for rebuild costs?

Insurance providers use rebuild costs to determine the level of cover needed to fully restore your property after significant damage or total loss. An inaccurate figure could result in underinsurance or higher-than-necessary premiums.

Do extensions increase the rebuild cost of a house?

Yes, extensions increase the total floor area and often add structural complexity, which can raise the rebuild cost. Any major property improvements should be reflected in updated insurance and valuation assessments.

How often should I update my home’s rebuild cost?

It is generally recommended to review rebuild costs every few years or whenever significant changes are made to the property. Rising construction costs and inflation can also affect rebuilding expenses over time.

Are listed buildings more expensive to rebuild?

Yes, listed buildings typically cost more to rebuild because they often require specialist materials, traditional construction methods, and compliance with heritage regulations. These factors can significantly increase project costs.

Can online rebuild cost calculators provide accurate estimates?

Online calculators can provide a useful starting point, but they may not account for unique property features, site conditions, or regional variations. Professional assessments usually deliver more accurate and reliable figures.

What factors have the biggest impact on house rebuild costs in the UK?

The most significant factors include property size, location, construction materials, design complexity, labour rates, site accessibility, and professional fees. Changes in construction market conditions can also influence rebuilding costs.

Conclusion

Estimating house rebuild costs is not something homeowners should leave to guesswork, especially when insurance cover, property planning, and major financial decisions are involved. The final figure can be shaped by several important factors, including the size of the property, construction materials, labour rates, site access, demolition work, professional fees, building regulations, and regional UK pricing differences. A simple online calculator can give a useful starting point, but it may not reflect property-specific details such as unusual layouts, listed-building requirements, poor ground conditions, or high-specification finishes. For a more accurate rebuild valuation, it is sensible to seek advice from a qualified surveyor, insurance valuer, or professional cost-assessment service that understands current construction costs. Keeping your insurance valuation up to date is just as important, because outdated figures can leave you underinsured if your home needs to be rebuilt after serious damage. Before making major property, renovation, or insurance decisions, getting expert guidance can give you clearer numbers, better protection, and more confidence in your next step.